Blank Rhode Island Promissory Note Template

In Rhode Island, individuals and businesses often engage in transactions requiring a form of written promise for the payment of a debt. This is where a Rhode Island Promissory Note form becomes essential. It acts as a legal document that outlines the terms under which one party promises to pay money to another. The form covers various crucial aspects, including the principal amount, interest rate, repayment schedule, and the consequences of default. It serves not only as a clear agreement between the parties involved but also as a legally binding document that can be enforced in court if necessary. Whether the promissory note is secured by collateral, which offers additional protection to the lender, or unsecured, greatly influencing the agreed-upon terms, understanding the contents and implications of this document is vital for both lenders and borrowers in Rhode Island.

Example - Rhode Island Promissory Note Form

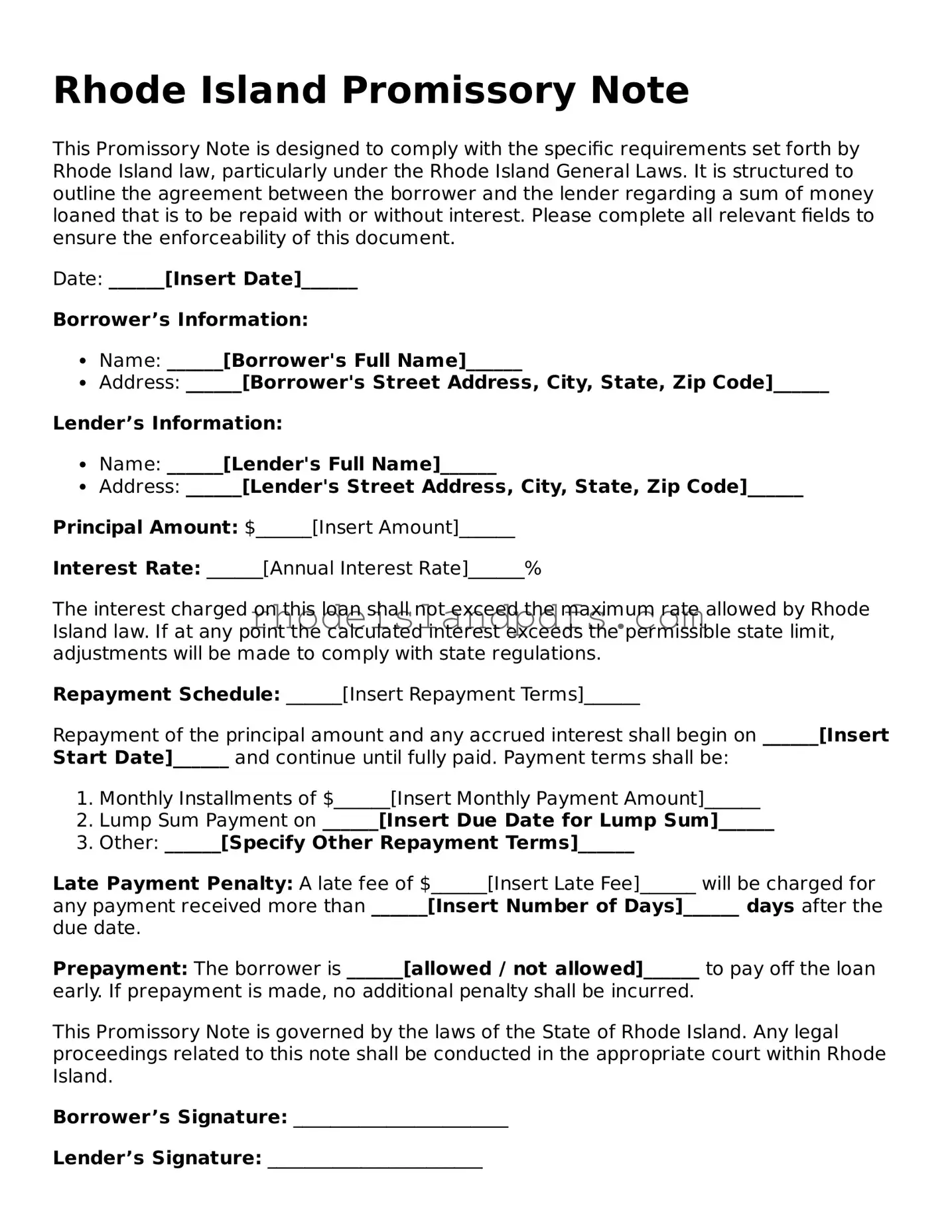

Rhode Island Promissory Note

This Promissory Note is designed to comply with the specific requirements set forth by Rhode Island law, particularly under the Rhode Island General Laws. It is structured to outline the agreement between the borrower and the lender regarding a sum of money loaned that is to be repaid with or without interest. Please complete all relevant fields to ensure the enforceability of this document.

Date: ______[Insert Date]______

Borrower’s Information:

- Name: ______[Borrower's Full Name]______

- Address: ______[Borrower's Street Address, City, State, Zip Code]______

Lender’s Information:

- Name: ______[Lender's Full Name]______

- Address: ______[Lender's Street Address, City, State, Zip Code]______

Principal Amount: $______[Insert Amount]______

Interest Rate: ______[Annual Interest Rate]______%

The interest charged on this loan shall not exceed the maximum rate allowed by Rhode Island law. If at any point the calculated interest exceeds the permissible state limit, adjustments will be made to comply with state regulations.

Repayment Schedule: ______[Insert Repayment Terms]______

Repayment of the principal amount and any accrued interest shall begin on ______[Insert Start Date]______ and continue until fully paid. Payment terms shall be:

- Monthly Installments of $______[Insert Monthly Payment Amount]______

- Lump Sum Payment on ______[Insert Due Date for Lump Sum]______

- Other: ______[Specify Other Repayment Terms]______

Late Payment Penalty: A late fee of $______[Insert Late Fee]______ will be charged for any payment received more than ______[Insert Number of Days]______ days after the due date.

Prepayment: The borrower is ______[allowed / not allowed]______ to pay off the loan early. If prepayment is made, no additional penalty shall be incurred.

This Promissory Note is governed by the laws of the State of Rhode Island. Any legal proceedings related to this note shall be conducted in the appropriate court within Rhode Island.

Borrower’s Signature: _______________________

Lender’s Signature: _______________________

PDF Specs

| Fact Name | Description |

|---|---|

| Definition | A Rhode Island Promissory Note is a legally binding document between a lender and a borrower, where the borrower agrees to repay a loan to the lender under specific terms. |

| Governing Laws | The form and enforcement of Promissory Notes in Rhode Island are governed by both federal laws and specific Rhode Island statutes. |

| Types | There are two main types: secured and unsecured. Secured notes are backed by collateral, while unsecured notes are not. |

| Interest Rate | In Rhode Island, the legal maximum interest rate without a written agreement is 21% or the maximum amount permitted under federal law. |

| Usury Limit | If the interest rate exceeds the legally established limit, it can be considered usurious, subjecting the note to potential penalties. |

| Prepayment | Borrowers in Rhode Island are generally allowed to prepay their debt without incurring a penalty, unless specifically stated otherwise in the promissory note. |

| Default | Upon default, the lender is entitled to pursue legal actions to enforce repayment, which may include taking possession of the collateral, if any. |

| Cosigners | A promissory note may include a cosigner, who becomes equally responsible for the loan repayment if the primary borrower defaults. |

| Release of the Note |

Steps to Writing Rhode Island Promissory Note

When it comes to formalizing a loan agreement between parties in Rhode Island, using a promissory note can be an effective way to detail the commitment. This legal document, while seemingly straightforward, requires careful attention as it outlines the loan's terms, including repayment schedule, interest rate, and what happens in the case of default. By clearly articulating these elements, both lender and borrower can safeguard their interests and reduce potential misunderstandings down the line. The steps below guide you through the necessary process to accurately fill out a Rhode Island Promissory Note form.

- Gather all relevant information including the loan amount, interest rate, payment schedule, and personal details of both the lender and borrower.

- At the top of the document, enter the date the promissory note is being created.

- Write down the full names and addresses of both the borrower and the lender to establish their identity and roles in the agreement.

- Specify the principal amount of the loan in U.S. dollars to clarify the exact amount of money being lent.

- Determine and input the interest rate annually (APR) that will be applied to the loan. This must comply with Rhode Island's usury laws to avoid illegal interest charges.

- Detail the repayment plan. Include how often payments will be made (e.g., monthly), the amount of each payment, and when the first payment is due. Additionally, note the final payment date by which the loan will be fully reimbursed.

- If applicable, describe any collateral that the borrower is using to secure the loan. This should include a clear description of the asset and its value.

- Outline the actions that will be taken if the borrower fails to make timely payments. This could include late fees, acceleration of the loan balance, or legal action.

- Both parties should carefully review the completed form to ensure all information is accurate and reflects their agreement.

- Lastly, the borrower and lender must sign and date the document. Witnesses or a notary public may also be required to sign, depending on local laws and regulations.

Once the Rhode Island Promissory Note is fully executed, it becomes a binding contract. It's important for both parties to keep a copy of the document for their records. Following these steps not only helps in clearly laying out the terms of the loan but also in protecting the rights and responsibilities of everyone involved. Remember, promissory notes are not just formalities but enforceable legal documents that can be used in court if necessary.

Key Facts about Rhode Island Promissory Note

What is a Rhode Island Promissory Note form?

A Rhode Island Promissory Note form is a legal document in which one party, known as the borrower, agrees to pay back a specified amount of money to another party, the lender. This form outlines the amount borrowed, interest rate, repayment schedule, and any other terms related to the loan. It serves as a legally binding contract between the two parties in Rhode Island, ensuring that the borrower commits to repaying the debt under the agreed-upon conditions.

How do I ensure my Rhode Island Promissory Note is legally binding?

To ensure that your Rhode Island Promissory Note is legally binding, it must contain critical elements such as the amount of money borrowed (principal), interest rate, repayment schedule, and the signatures of both parties involved. Additionally, both the lender and borrower must enter into the agreement willingly and with a clear understanding of the terms. Including witness signatures or getting the document notarized can further strengthen the document’s legal enforceability.

Does the interest rate on a Rhode Island Promissory Note have a maximum limit?

Yes, in Rhode Island, the interest rate on a promissory note does have a maximum limit. The law stipulates that lenders cannot charge an interest rate exceeding the legal limit, which is determined by state usury laws. The specific rate can vary, so it's important to check the current laws to ensure compliance. Charging an interest rate above the legal limit can result in penalties and make the promissory note unenforceable.

Can I modify a Rhode Island Promissory Note after both parties have signed it?

Yes, a Rhode Island Promissory Note can be modified after it has been signed, but any alterations require the agreement of both the lender and the borrower. This typically involves drafting an amendment to the original note or creating a new promissory note that supersedes the original. Both parties must then sign the amended document for the changes to be legally binding. Communication and consent are key when modifying any terms of the promissory note.

What happens if the borrower fails to repay the loan as agreed in the Rhode Island Promissory Note?

If the borrower fails to repay the loan according to the terms outlined in the Rhode Island Promissory Note, the lender has several legal remedies. The lender may demand immediate payment of the remaining loan balance, pursue legal action to enforce the agreement, or seek to attach the borrower's assets. The specific course of action depends on the terms of the promissory note and Rhode Island law. It's advisable for lenders to review their legal options and possibly consult with an attorney before proceeding with collection efforts.

Common mistakes

Completing the Rhode Island Promissory Note form can sometimes be challenging. There are common mistakes people tend to make which could lead to significant consequences. It's crucial to be precise and careful when filling out this document to avoid any future financial or legal misunderstandings.

- Not Specifying the Payment Plan Clearly: One of the most critical sections of the promissory note involves the repayment terms. A clear payment plan includes the amount, frequency, and duration of payments. When these details aren't defined precisely, misunderstandings can arise, leading to disputes. It's essential for both the lender and borrower to agree on these terms to ensure there are no ambiguities.

- Omitting the Interest Rate: Failing to include the interest rate is a common mistake. In Rhode Island, if an interest rate is not specified, the note might be subject to the state's default rate. However, specifying the rate helps in keeping the repayment expectations transparent. This omission can also affect the total amount to be repaid, potentially leading to disagreements between the parties involved.

- Neglecting to Include a Late Payment Policy: Many people forget to outline the consequences of late payments. Including a late payment policy not only ensures that there is a measure in place to deal with such situations but also encourages timely payments. Failure to include such a policy can lead to difficulties in managing late payments and enforcing penalties.

- Not Identifying the Parties Correctly: It's crucial to accurately identify all parties involved in the agreement by their full legal names. This identification includes any co-signers or guarantors. Misidentifying any party can void the agreement or complicate legal proceedings if the note is ever contested or defaults occur.

- Forgetting to Sign and Date the Document: Perhaps the simplest but most critical error is forgetting to have the document duly signed and dated by all parties involved. An unsigned promissory note is potentially unenforceable. The signature is a key element that indicates the agreement and consent of the terms laid out in the document by both the borrower and lender.

Being attentive and ensuring that these errors are avoided can save a great deal of time and prevent potential legal and financial conflicts. It's advisable to carefully review the promissory note form, or even better, consult with a legal professional to ensure that all sections are accurately completed. This careful attention helps in maintaining the validity of the agreement and protecting the interests of both parties involved.

Documents used along the form

When individuals or entities engage in lending or borrowing money in Rhode Island, the Rhode Island Promissory Note form is a fundamental document that outlines the repayment agreement. However, this form is often just one part of a suite of documents utilized to ensure clarity, legality, and the smooth process of the transaction. These related documents can vary based on the specific requirements of the loan, the relationship between the borrower and lender, and the presence of any collateral. Below is a list of other forms and documents frequently used alongside the Rhode Island Promissory Note to enhance the security and enforceability of the financial agreement.

- Loan Agreement: This comprehensive document provides detailed information about the loan terms, including but not limited to interest rates, repayment schedule, and the obligations of both parties. Unlike the Promissory Note, a Loan Agreement often includes more extensive clauses on dispute resolution and default.

- Security Agreement: If the loan is secured with collateral, this document is crucial. It grants the lender a security interest in a specific asset or property pledged by the borrower as security for the loan’s repayment.

- Mortgage Agreement: In real estate transactions, this document secures the loan against the purchased property. It details the rights and responsibilities of both parties and outlines the legal procedures for foreclosure in the event of default.

- Guaranty: This is a promise made by a third party, the guarantor, to repay the loan if the original borrower fails to do so. It provides an extra layer of security for the lender.

- Amendment Agreement: Should the terms of the original Promissory Note or related documents need to be modified, this document outlines the amendments agreed upon by all parties.

- Release of Promissory Note: After the loan is fully paid off, this document serves as proof that the borrower has fulfilled their financial obligations and that the lender releases them from further liability.

- Notice of Default: This document is used to formally notify the borrower that they have failed to meet one or more terms of the Promissory Note, such as missing a scheduled payment.

- Late Fee Agreement: If the lender allows for late payments, this document outlines the fees that the borrower will incur for not making payments on time.

Deed of Trust: Similar to a Mortgage Agreement, this document involves a third party, called a trustee, holding the title to the property until the loan is paid in full. It is commonly used in some states as an alternative to a mortgage. Subordination Agreement: This document is used to change the priority of liens against the collateral, with the lender agreeing that their claim to the asset will take precedence over other creditors.

The utilization of these documents, in conjunction with the Rhode Island Promissary Note, contributes to a legally binding and enforceable agreement that protects the interests of both the borrower and the lender. It is crucial for parties involved in such financial transactions to thoroughly understand these documents to ensure compliance and to minimize potential legal disputes. Consulting with a legal professional is advisable to navigate the complexities of these financial agreements effectively.

Similar forms

The Rhode Island Promissory Note form is similar to several other financial and legal documents in various ways. It is an agreement that involves a borrower promising to repay a sum of money to a lender under specified conditions. This form shares features with loan agreements, IOU documents, and mortgage notes. Each of these documents serves a specific purpose in the realm of finance and legal obligations related to borrowing and lending money.

Loan Agreement: A loan agreement is a comprehensive document that outlines the terms and conditions of a loan between a borrower and a lender. The Rhode Island Promissory Note form has similarities to a loan agreement in that both specify the amount of money being borrowed, the interest rate, and the repayment schedule. However, a loan agreement often contains more detailed provisions regarding the responsibilities and obligations of both parties, such as clauses on late payments, collateral, and default conditions.

IOU Document: An IOU (I Owe You) document is a simple acknowledgment of debt. This document is less formal than a promissory note and usually does not include detailed terms such as the interest rate and repayment schedule. The Rhode Island Promissory Note form is similar to an IOU in that both indicate an amount of money owed by one party to another. However, the promissory note is more binding and formal, including specific terms under which the debt will be repaid.

Mortgage Note: A mortgage note is a legal document that outlines the borrower's promise to repay a mortgage loan, allowing the lender to foreclose on the property if the borrower fails to meet the terms of repayment. The Rhode Island Promissory Note form is comparable to a mortgage note in that it is a promise to pay under specific conditions. However, while a mortgage note is secured by the property being financed, a promissory note may not always be secured by collateral and can cover various types of loans beyond real estate.

Dos and Don'ts

Filling out a Rhode Island Promissory Note Form requires careful attention to detail and an understanding of your legal obligations. To assist you effectively, here's a comprehensive guide outlining the dos and don'ts to keep in mind:

Do:Verify the accuracy of all details included, such as names, addresses, and the loan amount, to prevent any misunderstandings.

Clearly indicate the interest rate, ensuring it complies with Rhode Island's usury laws, to avoid any legal issues.

Outline the repayment schedule in detail, including due dates and the amount of each payment, to maintain a clear payment structure.

Specify the collateral, if any, securing the loan, which can provide legal recourse in case of default.

Include clauses concerning late fees and any other penalties to ensure the borrower is aware of the consequences of late payments.

Leave any sections blank, as incomplete forms can lead to disputes and a lack of enforceability.

Forget to have both the borrower and lender sign and date the form, as lack of signatures can question the validity of the agreement.

Following these guidelines will help ensure the promissory note is legally binding and enforceable in Rhode Island. This will provide both parties with a clear understanding of their rights and responsibilities, helping to avoid conflicts during the repayment period.

Misconceptions

When discussing the Rhode Island Promissory Note form, several misconceptions frequently emerge. Clearing up these misunderstandings is essential for both lenders and borrowers engaging in financial agreements within the state. Here are ten common misconceptions:

It needs to be complicated. Many people assume that legal documents, including promissory notes, must be filled with complex legal jargon. In reality, clarity and simplicity are key. The form should be straightforward, making sure all parties understand the terms without a legal dictionary.

Only banks can issue them. This is not the case. While banks and other financial institutions frequently issue promissory notes, individuals can also create and utilize them for personal loans, real estate transactions, or even between friends and family members.

A verbal agreement is just as binding. While oral contracts can be legally binding, a written promissory note provides a clear, enforceable record of the agreement and its terms. In the case of disputes, written evidence is far more reliable than memory.

It must be witnessed or notarized. Unlike some legal documents, a promissory note in Rhode Island does not require notarization or witnesses to be legally binding. However, having a neutral third party witness the signing can add an extra layer of protection for both parties.

The interest rate can be as high as agreed upon. Rhode Island law limits the maximum interest rate that can be charged in a promissory note. Charging an interest rate above this legal maximum can render the note usurious and legally void.

It's only for large sums of money. Promissory notes can be used for loans of any size. They're not limited to large financial transactions. Small loans between private individuals are just as valid reasons to create a promissory note.

It doesn't need to specify repayment terms. On the contrary, a promissory note should clearly outline the repayment terms, including the amount, due dates, and any installment payment details. Vague terms can lead to misunderstandings and legal disputes.

It's final and unmodifiable. While a promissory note is a binding legal agreement, the terms can be modified if both parties agree. Any changes should be documented in writing to maintain clarity and legal standing.

Electronic signatures aren't valid. Electronic signatures are legally recognized and can be just as binding as traditional ink signatures on paper. This flexibility can facilitate transactions, especially in today's digital world.

Filling out the form is all that's required. While completing the form is crucial, understanding and agreeing to its terms is equally important. Both parties should review the document carefully and consider seeking legal advice to ensure their rights and obligations are clear.

Correcting these misconceptions can lead to more secure and understandable financial agreements. Both lenders and borrowers will benefit from a clearer understanding of their rights and responsibilities under Rhode Island law.

Key takeaways

Filling out and using the Rhode Island Promissory Note form correctly is crucial for ensuring its enforceability and the protection of all parties involved. Here are key takeaways to consider:

- Understanding the form’s purpose is essential. A Promissuary Note is a legal document that outlines a loan's terms, including the repayment schedule, interest rate, and the consequences of non-payment.

- Ensure all parties have a clear understanding of the terms. Clarity prevents future misunderstands or disputes.

- The full legal names of the lender and borrower must be used in the document to avoid any ambiguity regarding the parties involved.

- Specify the loan amount in words and numbers to prevent alterations and ensure clarity.

- Clearly outline the repayment schedule, including due dates and the total number of payments. This detail helps both parties keep track of the obligations.

- The interest rate should be explicitly stated, and it must comply with Rhode Island’s usury laws to avoid being rendered void.

- Include clauses for late fees and consequences of default. This element provides a course of action if the borrower fails to meet the terms.

- If collateral is used to secure the loan, describe it clearly in the document. This description is crucial for secured loans.

- Both the lender and the borrower should sign the promissory note, and it's wise to have the signatures notarized to affirm the document's authenticity and the signatories' identities.

- Keep a copy of the promissory note in a safe place. Both the lender and the borrower should have copies to refer back to, ensuring they have proof of the agreement and its terms.

Adhering to these pointers will help in creating a comprehensive and legally sound Rhode Island Promissory Note, safeguarding the interests of both parties involved in the loan agreement.

Fill out Other Common Forms for Rhode Island

Rhode Island Notary Verification - Involving a simple process, this form elevates the legal credibility of a document by authenticating its signature.

Hold Harmless Letter - Educational institutions may require students and parents to sign a Hold Harmless Agreement for participation in extracurricular activities, minimizing the school's legal risk.